🔑 I've never seen a billion dollar deal collapse so fast

Welcome to The Business Buying Academy with Sieva Kozinsky. Here's what we have in store for you today:

- They lit $1.45 billion on fire. Here's what you can learn from them

- Warning to all business buyers

- My collection of business buying lessons

🔑 How to lose $1.45 billion in less than 2 years

The 1980s was a defining moment for business buying.

Many would call it the LBO Craze.

Leveraged buyouts (LBOs) were a new mechanism for buying companies that fueled a frenzy of acquisitions.

That frenzy was fueled by deregulation, easy credit, and a speculative appetite for high-risk, high-reward deals.

LBOs are buyouts, often done by private equity firms, where the buyer acquires a company using a lot of debt (typically 70-90% of the purchase price) secured against the target’s assets or cash flows, with minimal equity.

While many of the conditions that created the LBO craze are long-gone, there are plenty of lessons we can still learn today:

- Don't overpay for a business just because everyone else is

- Finance acquisitions responsibly; there is such a thing as too much debt.

- A good business can turn into a bad business with the wrong capital structure.

Many of these lessons might remind you of the bidding war for HVAC and other home service businesses today, financed aggressively with SBA loans.

Now let's just back to the 1980s.

If you want to understand the LBO Era, you need to understand the poster child of the time: The $25 billion RJR Nabisco LBO in 1988.

The defining book of the era, Barbarians at the Gate, is primarily about this deal. It's way too big of a story to tell today, but here's a quick summary:

The RJR Nabisco leveraged buyout (LBO), valued at $25 billion, was the largest and most iconic deal of the 1980s LBO craze. RJR Nabisco, a conglomerate spanning tobacco (R.J. Reynolds) and food (Nabisco brands like Oreo), became the target of a fierce bidding war after CEO F. Ross Johnson proposed a management-led buyout to take the company private. Private equity firm Kohlberg Kravis Roberts & Co. (KKR) ultimately won against Johnson’s group and others, including First Boston, with a bid of $109 per share in November 1988. The deal was financed with roughly 87% debt, including junk bonds arranged by Drexel Burnham Lambert, and only 13% equity.

But hundreds of other deals happened around the same time.

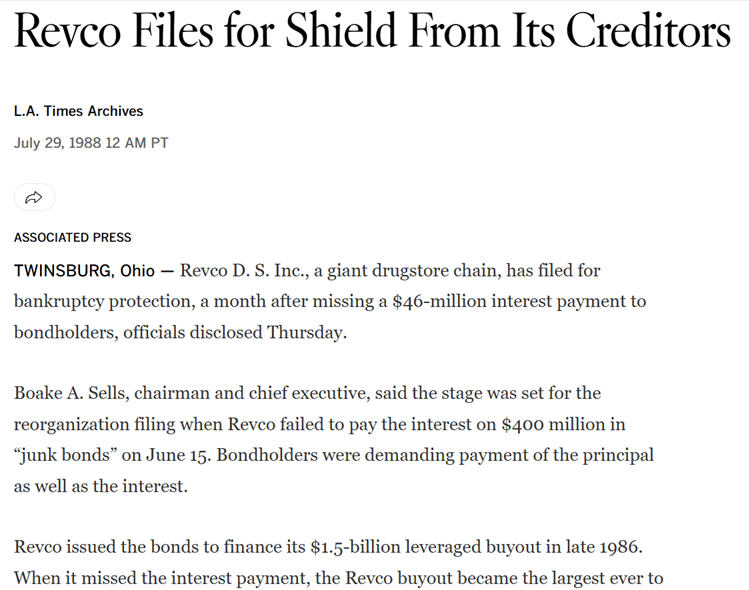

Today, I want to highlight one you probably haven't heard of: The $1.45 billion buyout of Revco, a discount drugstore chain.

This $1.45 billion deal exemplifies the high-stakes world of 1980s LBOs, where junk bonds and heavy debt fueled aggressive acquisitions but often led to spectacular failures.

Deal Overview

- Structure: The buyers offered Revco shareholders a 36% premium over market value, financed with a mix of:

- 31% senior debt

- 49% subordinated debt (much of it high-yield "junk" bonds)

- 19% equity from investors

- 1% equity from the management team.

This new structure quadrupled Revco's long-term debt from $309 million to about $1.3 billion 🚩🚩🚩

- Rationale: The LBO aimed to take the public company private, streamline operations, and capitalize on the growing pharmacy sector amid deregulation and retail expansion. In other words, the debt will pay for itself as management aggressively expanded the business.

Outcome

The deal collapsed within 19 months.

Revco defaulted on a $46.5 million interest payment in June 1988 and filed for Chapter 11 bankruptcy in July 1988.

Key factors included overestimated cash flows, aggressive inventory purges that disrupted sales, vendor distrust leading to tighter credit terms, and high interest burdens amid economic slowdowns.

Revco posted consistent net losses with no post-LBO profit margins. The business eventually reemerged from bankruptcy in 1992 but was later acquired by CVS in 1997 at a fraction of the LBO value.

Lessons:

- Debt is a powerful tool. It can multiple your returns, but it can crash your investment quickly.

- You can't always count on aggressive growth. Ask yourself if a deal will still work out even if the business doesn't grow in year 1 (many acquisitions, especially in SMB land, often don't).

🔑 Don't make this mistake when buying a business

Buying a business without getting a quality of earnings report is like buying a house without a home inspection. You’re taking a big bet without knowing what you’re buying, and it could be a disaster.

Even if the seller gives you all their financial statements, they often have very bad bookkeeping.

So, what should be in your QOE and financial due diligence package? Here's what today's sponsor Appletree says about their QOE reports:

✅ Proof of Cash

Are revenues real? We rebuild the last 1-2 years using bank statements to verify that reported earnings arrived in the bank account.

✅ Addbacks That Actually Make Sense

We normalize SDE or EBITDA with logic, not wishful thinking. The hand-waving. No “adjusting away” real costs just to make numbers look better.

✅ Working Capital Analysis

Avoid the “Post-Close Surprise” where you’re suddenly short $150k in working capital. We calculate what the business needs to operate smoothly.

✅ Forward Looking Projections

We model post close cash flow and debt service coverage under flat, growth, and decline scenarios – so you know how risky the deal really is.

If you’re sending out LOI’s or nearing a deal, don’t go in blind. Talk to Appletree for a pragmatic, thorough Quality of Earnings report – built by people who’ve bought businesses themselves.

🔑 Want to buy a business? Pay attention

I've been interviewing dozens of people over the last year.

My goal: Assembling the greatest collection of business buying lessons from people who have done it.

Their businesses range from $1 million accounting firm to $100 million manufacturing businesses, and everything in between.

We've got self-funded searchers, private equity partners with billions under management, and horizontal holding company owners looking to add the next great business to their portfolio.

No matter what type of business you're looking to buy, I probably have a story for you. Check out the interview below.

Have a great day,

Sieva

P.S. - Are you hiring? Get started with top global talent from Somewhere (I'm a customer and investor)

Disclaimer: nothing here is investment advice. Please do your own research. The information above is just for information and learning.